Deep Dive 9: MercadoLibre (MELI) - The Technologist

Lede

MercadoLibre is Latin America’s largest online commerce and fintech ecosystem – essentially the region’s “Amazon plus PayPal” combined in one company (Source).

It operates a massive marketplace for buyers and sellers across 18 countries, alongside a suite of services like payments, shipping, and credit that enable safe and convenient online shopping (Source).

MercadoLibre’s business spans a marketplace, fintech services, logistics, and advertising, creating a full ecosystem for commerce in Latin America.

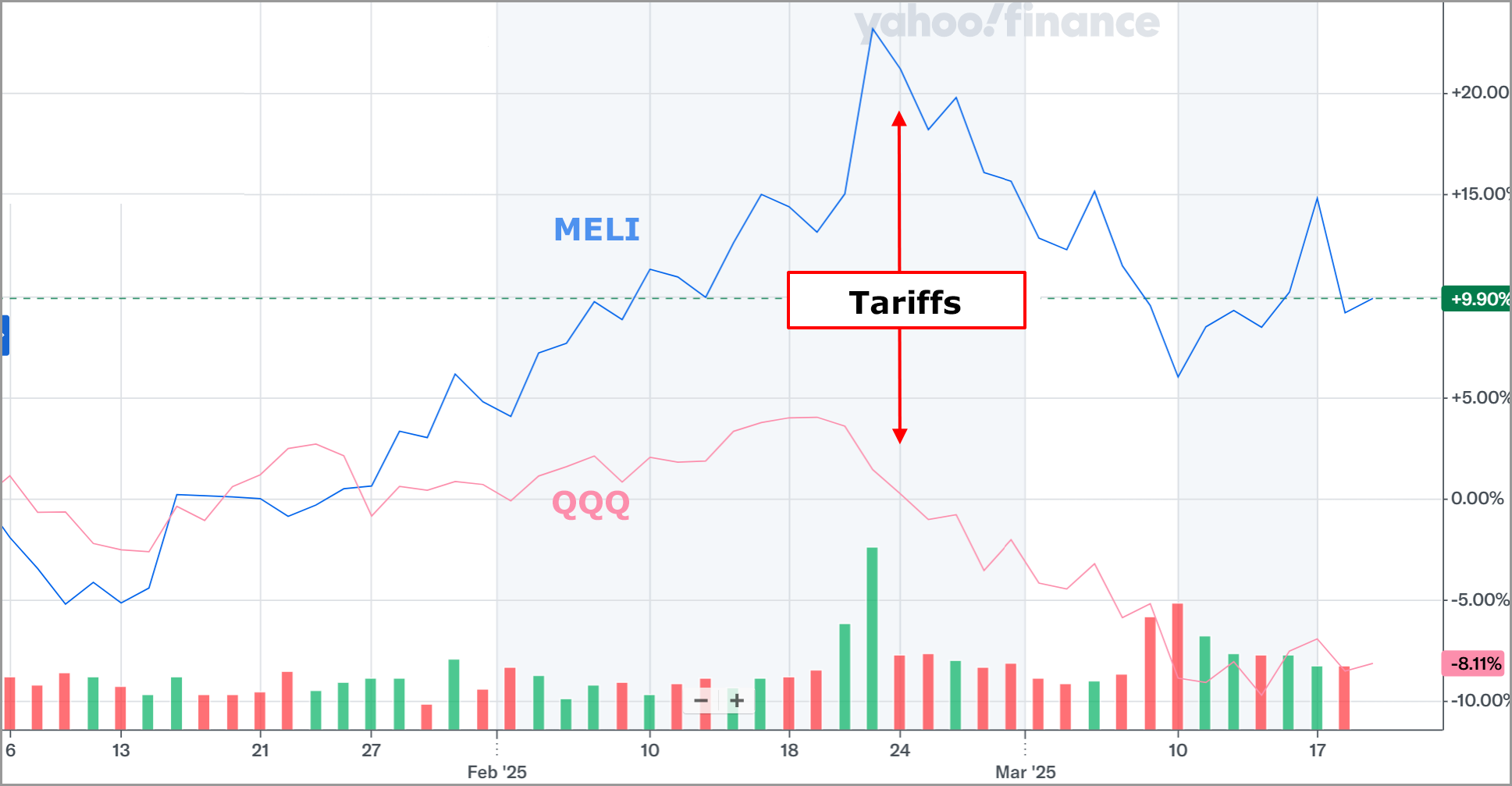

In today’s trying times, with tariff wars launching, MELI may not only be a safe haven, but may benefit from Trump tariff wars (more on that later in this dossier).

But rather than rely on an intellectual argument, we can look at the performance of MELI versus the NASDAQ 100 (QQQ) year to date, and at least for now, the market believes tariffs are bad for the US and good (or less bad) for MELI.

Founded in 1999 in Argentina, MercadoLibre has grown into the most valuable company in Latin America (around a $100 billion market cap) by solving the region’s unique e-commerce challenges and “democratizing” access to digital commerce and payments (Source).

MercadoLibre (often nicknamed MELI) is the dominant e-commerce platform in Latin America, serving as an online marketplace where millions of users buy and sell goods every day.

It also runs one of the region’s leading financial technology platforms, offering digital payment services and credits to people and businesses who often lacked access to traditional banking.

Together, its commerce and fintech businesses have transformed how Latin Americans shop and pay, making MercadoLibre a central part of the region’s digital economy.

The company’s rise is frequently compared to Amazon’s in the U.S., but MercadoLibre built its success by tailoring solutions to Latin America’s needs – from developing trust in online transactions to building its own delivery network in countries with challenging infrastructure (Source).

Big Idea; Big Reality: What if there is a US Recession?

• A US recession mostly affects the US economy, not Latin America.

• MercadoLibre’s performance is driven by local Latin American fundamentals, making it less sensitive to US economic cycles.

While a US recession can create global market volatility, MercadoLibre’s core business is tied to the e-commerce and fintech trends in Latin America.

Tell It to Me Like I’m 11-years Old

Imagine a huge mall on your computer or phone where you can find toys, clothes, electronics – anything you want.

MercadoLibre is that mall for Latin America.

People from different countries use it to buy and sell things online, just like trading cards in a playground, but with safe delivery to your home.

Because not everyone has a bank or credit card, MercadoLibre created MercadoPago, which is like a magical piggy bank on your phone.

MercadoPago lets you pay for stuff online or in stores without cash – you can just tap and pay.

They even help people who need some money by giving small loans (through MercadoCrédito), kind of like when a friend lends you lunch money and you pay them back later.

MercadoLibre also has its own delivery trucks and warehouses, so when you order something, they quickly pack it and bring it to your door.

In short, MercadoLibre makes shopping easy and fun for millions of people, by helping them buy what they need and pay for it even if they don’t have traditional banks.

Preface

Easy Button:

• MercadoLibre’s business spans a marketplace, fintech services, logistics, and advertising, creating a full ecosystem for commerce in Latin America.• The company’s revenue is geographically diversified – Brazil is its largest market (about half of revenue), followed by Mexico and Argentina, with each major segment (Commerce and Fintech) contributing a significant share (Source).

• By integrating online shopping with payments, shipping, and credit, MercadoLibre has multiple streams of income – from marketplace transaction fees and shipping fees to payment commissions, interest on loans, and advertising sales.

MercadoLibre’s core mission is to “democratize commerce and payments” in Latin America by providing a complete tech platform for online buying, selling, and financial services.

Practically, this means the company operates several interlocking business units that reinforce each other: an e-commerce marketplace (Mercado Libre means “free market” in Spanish), a payments arm (MercadoPago), a lending arm (MercadoCrédito), a logistics service (MercadoEnvíos), an advertising platform (MercadoAds), and even a storefront solution (MercadoShops) for merchants.

Each unit generates revenue in different ways.

For example, the marketplace earns commissions and listing fees from sellers, MercadoPago earns fees from processing payments and money transfers, and MercadoEnvíos earns fees for shipping services – though these logistics and payment revenues often have lower margins, they boost overall transaction volume and trust on the platform (Source).

Meanwhile, newer services like MercadoAds are high-margin, allowing MercadoLibre to monetize its user traffic with advertising akin to how Amazon does.

Geographically, MercadoLibre has a broad Latin American footprint, but its revenue is concentrated in a few key countries:

Brazil is by far the largest market – in 2023 it accounted for roughly 52% of MercadoLibre’s $14.5 billion net revenue (Source).

Mexico has rapidly grown to around 20% of revenue, and Argentina (the company’s birthplace) contributes about 22%, with the remaining ~5% coming from other countries in the region (Source).

This spread shows that while MercadoLibre dominates across Latin America, it particularly leans on Brazil’s huge e-commerce base and Mexico’s emerging market, even as it navigates Argentina’s challenging economy.

By business segment, MercadoLibre breaks out its revenue into Commerce and Fintech.

Initially, the Commerce segment (marketplace, ads, first-party sales, etc.) was the majority of revenue, but the fintech segment (MercadoPago and related financial services) has rapidly expanded – by 2024 fintech was contributing roughly 40% of total revenues, up from just 20% a few years prior (Source).

This balance reflects how integral payments and financial services have become to MercadoLibre’s ecosystem.

The company effectively leverages e-commerce as a gateway to offer banking-like services to users, generating additional revenue from payment processing fees, wallet balances (earning interest), and loan interest via MercadoCrédito.

In summary, MercadoLibre’s business model is a virtuous cycle: the more people use its marketplace, the more payments flow through MercadoPago and packages through MercadoEnvíos; the more sellers grow, the more they invest in ads or need credit; the better the fintech and logistics services, the more attractive the marketplace becomes.

This integrated approach has positioned MercadoLibre as a one-stop-shop for commerce, capturing value at multiple points of the transaction process.

Core Business Analysis

Easy Button:

• E-commerce (Marketplace & Logistics) – MercadoLibre’s marketplace connects millions of third-party sellers with buyers, supported by its own fulfillment and delivery network (MercadoEnvíos) that handles ~95% of packages and offers fast shipping across Latin America (Source).

• Fintech (Payments & Credit) – Through MercadoPago, users can pay online or in-store, send money, and even save or borrow; this has evolved into a full financial ecosystem with 61 million monthly active users and a $6.6 billion credit portfolio as of Q4 2024 (Source).

• Advertising – MercadoLibre is ramping up MercadoAds, allowing sellers and brands to promote products on its platform; this high-margin business grew ~41% YoY in Q4 2024 and now represents about 2% of the gross merchandise volume (signaling huge upside potential) (Source).

• Offline-to-Online Expansion – The company bridges physical commerce with digital: it provides point-of-sale payment solutions (like QR codes and card readers) to brick-and-mortar merchants and has a network of pickup/drop-off locations (MELI Places) at partner stores and gas stations, integrating offline shoppers and sellers into its online ecosystem (Source).

E-commerce Segment (Marketplace & Fulfillment): The marketplace is MercadoLibre’s historical core.

It operates mostly as a third-party (3P) marketplace where independent sellers list products, and MercadoLibre earns a commission on each sale (plus optional listing upgrades).

Over time, MercadoLibre also added some first-party (1P) sales (buying and reselling inventory itself) in certain categories to ensure key products are available – a strategy similar to Amazon’s mix of marketplace and direct sales (Source).

A critical element of the marketplace is the fulfillment and delivery infrastructure.

Through MercadoEnvíos, the company offers end-to-end logistics for sellers: storage in fulfillment centers, packing, shipping, and last-mile delivery.

In fact, MercadoLibre went from handling 8% of deliveries in-house in 2018 to 95% of all shipments by Q3 2024, after years of heavy investment in warehouses, fleet (including its own cargo aircraft), and local delivery partnerships (Source).

This logistics network is a major competitive advantage in a region where infrastructure can be unreliable.

Faster, reliable shipping builds customer trust – by late 2024 about half of all orders were delivered within 24 hours in major cities, far outpacing competitors’ speeds in Brazil and Mexico (Source).

MercadoLibre’s marketplace is structured to encourage trust and convenience: it offers buyer protection, a robust review system, and a loyalty program called MercadoPuntos (similar to Amazon Prime’s perks) where users earn points from purchases or using MercadoPago, unlocking benefits like free shipping and discounts on streaming services.

By addressing local pain points (for example, allowing cash-on-delivery or store pickup for those without reliable home addresses), MercadoLibre has brought tens of millions of Latin Americans into e-commerce.

In Q4 2024, the platform had 67 million unique active buyers (24% more than a year prior) and facilitated the sale of off 27% more items year-on-year, showing both user growth and higher engagement (Source).

Big Idea; Big Reality: These 24% more buyers and 27% more items, delivered 50% more GMV in 2024 in constant currency, but, of course, Latin America does not live in a world of constant currency.

The marketplace’s Gross Merchandise Volume (GMV) – the total value of goods sold – reached $14.5 billion in Q4 2024 alone (Source).

Notably, GMV growth in USD was a modest 8% that quarter (due to currency devaluations), but on a local currency (FX-neutral) basis it was over 50% YoY, reflecting strong underlying demand (Source).

To make delivery more convenient, MercadoLibre has expanded MELI Places, a network of locations (like corner shops, gas stations, and other retail partners) where buyers can pick up packages or sellers can drop off items to ship.

This extends MercadoLibre’s reach into neighborhoods, reducing last-mile costs and providing flexibility for customers who aren’t at home for deliveries.

In parallel, MercadoLibre’s logistics team continues to open new fulfillment centers (10 new warehouses were added in 2024 alone) to increase storage capacity near key urban areas (Source).

By controlling so much of the supply chain, MercadoLibre ensures that even sellers who are small or scattered can offer Prime-like delivery speeds through its platform – reinforcing a cycle where more buyers come for the convenience, which then attracts more sellers.

Payments and Fintech (MercadoPago & MercadoCrédito): MercadoPago was introduced in 2003 as a built-in payment solution to address the lack of trust and low credit card penetration in MercadoLibre’s early days (Source).

Today, MercadoPago has grown into a fintech powerhouse that not only processes payments for purchases on MercadoLibre’s marketplace but also operates far beyond it.

Consumers can use MercadoPago as a digital wallet to pay utility bills, top up mobile phones, transfer money to friends, or scan QR codes to pay in physical stores.

Merchants (even those not selling on MercadoLibre) use MercadoPago’s point-of-sale tools – for instance, small shops can accept card payments via MercadoLibre’s smartphone card readers or QR code system, turning cash transactions into digital ones.

This offline expansion is significant: one can now walk into many cafés or kiosks in Buenos Aires or São Paulo and pay via MercadoPago QR code, linking the offline economy into MercadoLibre’s ecosystem.

By late 2024, MercadoPago had 61 million monthly active users across its services, a 34% jump from the previous year (Source).

MercadoPago generates revenue through payment processing fees on transactions, fees on withdrawals, and also via the float on customer balances (similar to how PayPal or Square earn interest on customer funds).

In some countries, MercadoPago offers a savings account feature (Mercado Fondo) where users can park money and earn interest, which has driven the platform’s assets under management to about $10.6 billion by Q4 2024 (up 129% YoY) (Source).

Additionally, MercadoLibre’s fintech arm extends into credit via MercadoCrédito.

Starting by offering working capital loans to marketplace sellers and installment plans to buyers, it has grown into a sizable lending operation.

At the end of 2024, MercadoLibre’s credit portfolio reached $6.6 billion, a 74% year-over-year increase (Source).

These loans are often short-term and high-frequency (e.g. financing a purchase or a small business loan for inventory) and MercadoLibre leverages its rich data on transactions to underwrite them.

The credit business earns interest income, contributing about 20% of consolidated revenues in 2024 according to analysts (Source).

While offering credit boosts sales on the platform and adds another revenue stream, it also introduces risk from potential defaults – something MercadoLibre manages by adjusting credit limits and using advanced scoring models gleaned from user data.

One notable aspect of MercadoPago is its role in financial inclusion.

In Latin America, roughly 122 million adults were unbanked as of 2021 (about 26% of the adult population) (Source).

MercadoPago provides many of these people a first entry point into the formal financial system – users can deposit cash into their MercadoPago account at convenience stores and then transact online, or accept digital payments for their small business without a traditional bank.

This broadens MercadoLibre’s reach and creates loyalty: a user who uses MercadoPago for daily transactions is more likely to shop on MercadoLibre, and vice versa.

The synergy is evident – as more people shopped on MercadoLibre, Total Payment Volume (TPV) flowing through MercadoPago has exploded (including off-platform usage).

By integrating fintech so tightly, MercadoLibre not only earns additional revenue per user but also makes its ecosystem stickier, since having a MercadoPago balance or loan gives users reason to keep coming back.

Advertising Business (MercadoAds): MercadoLibre has begun to monetize the massive user traffic on its platform through advertising, following a playbook similar to Amazon’s ad business.

MercadoAds allows sellers and brands to pay for sponsored product listings, banner ads, and search placement on MercadoLibre’s website and app.

For example, a seller can sponsor their product to appear at the top of search results for relevant keywords, or a consumer brand can buy display ads to increase visibility. This business is still relatively nascent for MercadoLibre but growing very quickly.

In 2024, advertising revenue was about $1 billion (roughly ~5% of total revenues) and climbing – in the fourth quarter alone, ad revenue grew 41% year-over-year, outpacing overall GMV growth (Source).

Advertisements represented ~2.1% of MercadoLibre’s GMV in Q4 2024, up from about 1.7% a year prior (Source).

There is substantial room for this to grow – by comparison, Amazon’s ads are ~5% of its GMV and contribute a hugely profitable revenue stream (Source).

The attractiveness of MercadoAds lies in its extremely high margins.

Operating an ad platform has minimal incremental cost – once the system is built, each extra ad sold is mostly pure profit.

MercadoLibre indicated that marketplace ads could have 70-80% EBITDA margins at scale (Source).

Thus, expanding advertising not only diversifies MercadoLibre’s revenue but significantly boosts profitability.

The strategy is still in early innings: MercadoLibre is improving its ad targeting and tools, educating sellers on the benefits of advertising (many Latin American merchants are new to e-commerce advertising), and likely will introduce more ad formats.

As e-commerce penetration rises, brands will increasingly treat MercadoLibre as a key marketing channel, similar to how they budget for Google or Facebook, which positions MercadoAds as a future growth and margin driver.

It’s worth noting that MercadoLibre deliberately kept advertising low-key for years to focus on user experience, only scaling it up once the platform reached critical mass.

Now, with over 100 million annual buyers on the platform (Source), the opportunity to generate “easy” revenue from ads is huge.

The challenge will be to grow ads without cluttering the site or hurting conversion rates – a balance Amazon has managed well.

MercadoLibre’s management has signaled they are just scratching the surface of ad monetization, suggesting this segment will become far more significant in the next few years.

Offline-to-Online Expansion: A key aspect of MercadoLibre’s strategy is capturing the offline retail and financial activity and bringing it onto its platforms.

This manifests in a few ways. First, as mentioned, MercadoPago extends to physical stores via QR payments and Point-of-Sale (POS) devices.

By supplying small merchants with its own card readers (often little mobile POS dongles) and integrating with QR code standards, MercadoLibre turns brick-and-mortar sales into MercadoPago transactions.

Every time someone buys a cup of coffee or groceries using MercadoPago, that’s offline commerce flowing through MercadoLibre’s system (generating a small fee and reinforcing user habit).

In countries like Argentina and Brazil, MercadoPago has become one of the top payment methods in physical retail for certain segments, rivaling cash.

This not only grows MercadoLibre’s fintech user base but also serves as a funnel – a shop owner using MercadoPago may eventually consider listing products on MercadoLibre’s marketplace, or a shopper who trusts MercadoPago offline might be more inclined to shop online.

Secondly, MercadoLibre has experimented with blending offline and online shopping experiences.

It has opened a few concept stores and kiosks where top products are showcased and customers can get help ordering online.

More significantly, its Mercado Shops product allows existing offline retailers (or independent entrepreneurs) to create their own branded online storefronts using MercadoLibre’s infrastructure.

Big Idea: Mercado Shops is akin to a Shopify-like solution: a merchant can build an online store that is separate from the MercadoLibre marketplace but still leverages MercadoLibre’s payments, logistics, and traffic channels (Source).

This is aimed at helping established brands or retailers go online without leaving the MercadoLibre ecosystem.

While MercadoLibre hasn’t publicly broken out Mercado Shops data (it’s relatively quiet about it), third-party estimates suggested there are tens of thousands of active stores using it (Source).

Essentially, MercadoLibre is saying to retailers: “use our tools to sell online (on your own terms) and we’ll still handle your payments and shipping.”

It’s another way to capture market share of e-commerce, even if not directly through the main MercadoLibre site.

Additionally, by partnering with gas stations, convenience store chains, and courier points for its MELI Places pickup/drop-off network, MercadoLibre blurs the line between online and offline retail.

Customers can place an order online and pick it up at a familiar local shop, which is important in areas where home delivery is less practical or where consumers prefer the security of picking up goods at a known location.

For sellers, these locations serve as drop-off points that feed into MercadoLibre’s logistics network, meaning a person running a business from their home can simply drop parcels at a nearby kiosk rather than arranging a pickup.

This integration reduces friction in the e-commerce process and makes online commerce accessible even to customers who aren’t home-bound or who don’t have a reliable delivery address.

In summary, MercadoLibre’s offline-to-online initiatives are about extending its reach: turning cash-based, in-person transactions into digital ones within its ecosystem, and allowing traditional retail participants to plug into the online boom.

This omnichannel approach strengthens MercadoLibre’s moat, because it operates at many touchpoints of a consumer’s life (online shopping, offline purchases, financial services), making it harder for competitors to offer a similarly comprehensive value proposition.

Competitive Landscape

Easy Button:

• Global Rivals: MercadoLibre’s biggest global competitors in the region are Amazon (which is aggressively expanding in Brazil and Mexico) and, to a lesser extent, Shopee (Sea Limited’s e-commerce arm, which entered Brazil in 2019) – these giants bring deep pockets and expertise, forcing MELI to continuously up its game (Source).

• Local Competitors: In Brazil, traditional retailers like Magazine Luiza (Magalu) and Americanas have developed their own e-commerce marketplaces, and in fintech, players like Nubank, PagSeguro, and StoneCo compete for digital payments and lending – though none match MercadoLibre’s integrated ecosystem yet.

• SWOT Analysis:

Strengths – MercadoLibre’s network effect, localized know-how, and end-to-end logistics/fintech integration give it a formidable moat.

Weaknesses – Heavy reliance on a few countries (macro risk) and thinner margins in payments/logistics segments.

Opportunities – Growing internet penetration, untapped fintech users, and scaling high-margin ads.

Threats – Big-tech entrants (Amazon, Alibaba), aggressive local startups, and regulatory changes that could level the playing field or restrict operations.

MercadoLibre stands as the market leader in Latin American e-commerce, but it faces a mix of global heavyweights and nimble local players vying for a piece of the fast-growing market.

According to industry estimates, MercadoLibre controls roughly 25% of all Latin America e-commerce market share – the crown it has to defend (Source). Here’s a breakdown of key competitors:

Amazon (U.S. based global competitor): Amazon is MercadoLibre’s most direct global rival, especially in Brazil and Mexico.

Amazon entered Latin America later (around 2014 in Brazil, initially just with books, and ramping up around 2017-2019 with broader retail and Prime) and has since become the second-largest e-commerce player in Brazil by GMV (Source).

Amazon brings to the table its world-class logistics expertise, an enormous war chest to invest in warehouses and services, and the allure of Amazon Prime’s benefits (free shipping, streaming video/music, etc.) which it launched in Mexico and Brazil.

In Mexico, Amazon actually briefly overtook MercadoLibre in e-commerce traffic around 2020, leveraging its U.S.-Mexico supply chain and brand recognition.

Amazon’s strengths include a very advanced technology platform, global seller base (many Chinese manufacturers sell on Amazon into Mexico/Brazil), and AWS infrastructure (even MercadoLibre uses AWS for cloud services) (Source).

However, MercadoLibre has so far held its ground by virtue of its deep local integration – for example, Amazon cannot easily replicate MercadoPago or the ubiquity of MercadoLibre’s local pickup networks.

Big Idea; Big Reality: Still, Amazon is in Latin America for the long haul, steadily building fulfillment centers and courting local sellers.

The competition between MercadoLibre and Amazon is often likened to a chess match: MercadoLibre knows the local board better, but Amazon’s global experience and resources make it a constant strategic threat.

Shopee (Sea Limited (SE), Singapore-based): Shopee launched in Brazil in 2019 and expanded to other Latin countries in a bid to transplant its Southeast Asia playbook.

It gained traction through a gamified shopping experience – integrating games, daily rewards, and its parent company’s (Garena) popular mobile game Free Fire to acquire users (Source).

Shopee’s strategy involved heavy discounting, free shipping subsidies, and focusing on low-cost goods (often shipped directly from China) to undercut incumbents.

This “growth at all costs” approach saw Shopee quickly become a top shopping app by downloads and engagement in Brazil.

However, Shopee hit speed bumps: in 2022, amid rising losses, it pulled out of Argentina and scaled back in Chile, Colombia, and Mexico, consolidating focus mainly on Brazil with a cross-border model elsewhere (Source).

In Brazil, Shopee remains a meaningful competitor for MercadoLibre in the low-end segment – it’s popular among bargain hunters and younger users, thanks to its fun app experience (flash sales, mini-games) and cheap items.

Shopee’s weakness is its reliance on cross-border shipments for many products, meaning longer delivery times and potential customs hassles.

Big Idea; Big Reality: MercadoLibre’s advantage of fast local delivery stands in stark contrast to a typical Shopee order that might take weeks from China.

In fact, recent import tax changes in Mexico and Brazil (discussed later) target the very loopholes Shopee and similar platforms use.

As Sea Limited has cut back on aggressive expansion, MercadoLibre has some breathing room, but Shopee proved that global entrants can capture Latin American mindshare quickly with the right formula – a warning that MercadoLibre can’t be complacent, especially if Shopee reinvests or if another Asian player tries again.

AliExpress (Alibaba, China-based): Alibaba’s AliExpress has been present as a cross-border e-commerce option in Latin America for over a decade, quietly building a user base for ultra-cheap goods shipped from China.

While AliExpress is not a full-service local operator (no local warehouses – it’s purely international shipping), it became popular for products like electronics accessories, fashion, and gadgets due to rock-bottom prices.

In markets like Chile or Peru, where MercadoLibre’s presence is smaller, AliExpress filled a niche for cost-conscious consumers willing to wait for international delivery. Alibaba also made some investments in the region (for example, it partnered with Argentine postal service and others to improve deliveries).

Still, AliExpress remains a niche competitor in the sense that it doesn’t offer the integrated payments or fast shipping; it competes mainly on price and product variety from Chinese manufacturers.

MercadoLibre competes with AliExpress by leveraging its faster shipping and by onboarding local merchants (and Chinese sellers) to sell directly on MercadoLibre with inventory in-country.

Big Idea; Big Reality: Given global trade dynamics, AliExpress will always siphon some low-end demand, but it hasn’t evolved into a comprehensive local threat.

Local E-commerce Champions (Brazil & Others): MercadoLibre also contends with strong local retail companies that have gone digital.

In Brazil, Magazine Luiza (Magalu) and Via (formerly Via Varejo, owner of Casas Bahia) are notable examples.

Magalu in particular has executed a “digital transformation” – from a brick-and-mortar retailer into a tech-savvy e-commerce player with its own marketplace, fintech offerings, and even a developing super-app.

It acquired multiple startups (logistics, fintech, ads) to bolster its platform.

Big Idea; Big Reality: Magalu’s competitive edge is its physical store network (hundreds of stores nationwide) which it uses for omni-channel services (buy online, pick up in store) and its familiarity to Brazilian consumers.

Magalu’s marketplace has attracted sellers by promises of integration with its stores and heavy marketing.

That said, Magalu ran into challenges with profitability and an economic downturn, and an accounting scandal hit another rival (Americanas) in early 2023, which reduced some local competition.

Americanas (and Submarino/Shoptime under its umbrella) was once a major e-commerce player but its bankruptcy proceedings have impaired its operations, indirectly benefiting MercadoLibre in the short term.

In Mexico, a local competitor is Claro Shop (backed by Carlos Slim’s América Móvil) and Liverpool (a department store with a growing online arm), but none approach MercadoLibre’s scale.

MercadoLibre’s broad catalog and superior tech have generally kept it ahead of these local attempts, but it closely watches them – especially Magalu, which is often dubbed a Brazilian “super app in the making” for integrating content, fintech, and shopping in one app (Source).

Fintech Competitors: On the fintech side, competition is intense and comes from specialized players.

Nubank, a Brazilian digital bank, has tens of millions of customers and offers free checking accounts, credit cards, and more – becoming Latin America’s most valuable bank by market cap.

While Nubank isn’t an e-commerce company, it competes for the same fintech users that MercadoPago targets with digital wallets and credit.

So far, MercadoPago and Nubank seem to be carving out slightly different niches (MercadoPago focusing on payments within commerce, Nubank on banking services), but convergence is possible (e.g., Nubank could push a marketplace, and MercadoPago offers savings and loans already).

Other notable fintech rivals include PagSeguro and StoneCo in Brazil – these started as point-of-sale payment providers for merchants (with cheap card terminals) and have expanded into digital accounts and lending.

They compete directly with MercadoPago in offline merchant acquiring.

While MercadoPago has the advantage of the MercadoLibre platform’s volume, PagSeguro/Stone have deeply penetrated small businesses by selling millions of payment terminals over the years.

Additionally, traditional banks in various countries have improved their digital offerings and governments have introduced systems like Brazil’s Pix (an instant bank transfer system that’s free and ubiquitous) which, while not a “company competitor,” affects MercadoPago usage (Pix has become a popular alternative to card or wallet payments for peer-to-peer transfers) (Source).

MercadoLibre responds by integrating these systems (e.g., you can use Pix within MercadoPago) and emphasizing services beyond basic transfers (like offering credit, insurance, etc., via its app).

In the advertising space, MercadoLibre’s competition is basically the broader digital ad market – Google, Facebook (Meta), etc., which dominate online ad spending in LatAm.

For a merchant deciding where to advertise, they might weigh buying MercadoLibre sponsored ads versus Facebook Ads or Google search ads.

As MercadoLibre’s ad platform proves its ROI for sellers, it will pull more budget away from those external channels. This is more an indirect competition dynamic but important for MercadoAds growth.

SWOT Analysis vs Competitors

- Strengths: MercadoLibre’s key strength is its integrated ecosystem and first-mover advantage.

It has spent over two decades building trust with users, a brand synonymous with online shopping, and local operational know-how (such as handling cash payments, navigating local regulations, high-inflation economies, etc.).

Its ecosystem (marketplace + payments + logistics + credit + loyalty) is a self-reinforcing moat that global rivals find hard to replicate quickly.

For example, Amazon has great logistics but no equivalent of MercadoPago in LatAm; fintechs have apps but no giant commerce platform to drive adoption.

MercadoLibre also benefits from network effects – it has the largest pool of buyers which attracts the most sellers, and vice versa, making it hard for newcomers to reach the same scale of product selection or user base.

Another strength is localization and cultural fit: MercadoLibre is a Latin American company “built by Latin Americans for Latin Americans,” giving it an edge in understanding consumer behavior and pain points (as one executive put it, they tailored solutions for a cash-based society and complex geographies) (Source).

Finally, recent financial performance shows strengthening operational efficiency and profitability, which means MercadoLibre can now reinvest heavily in innovation or customer incentives to fend off competitors, something it might have struggled with years ago when profits were thin.

- Weaknesses: One of MercadoLibre’s weaknesses relates to its exposure to Latin American macroeconomic volatility (more on that in a later section), but in competitive terms this means its business can be erratic in dollar terms – whereas a global player like Amazon can offset a weak Brazil performance with strength in other regions, MercadoLibre is all-in on LatAm.

Another weakness is that some of MercadoLibre’s services (payments, logistics) are lower margin or even cost centers.

For example, offering free/cheap shipping and low payment fees is essential to stay competitive, but these can drag margins relative to a pure tech or marketplace model.

If competitors force a price war (say Amazon offers free shipping extensively or fintech rivals drive payment fees toward zero), MercadoLibre’s profitability could be more pressured given it operates these costly infrastructure-heavy segments.

Additionally, MercadoLibre historically has had a lower penetration in certain categories like high-end brands or groceries, partly because it started with a C2C and SME seller focus.

Amazon and local retailers could exploit this by partnering with big global brands or supermarkets to dominate those segments.

MercadoLibre is trying to overcome this (for instance, attracting official stores of Nike, Apple, etc., and rolling out MercadoLibre Supermercado for groceries), but it’s an area it cannot claim clear supremacy yet.

Lastly, in fintech, while MercadoPago is hugely popular for payments, it is not (yet) a full-service bank – competitors like Nubank offer a broader banking suite.

MercadoLibre might need to invest more in financial services (like insurance, investments, deposits) to prevent fintech customers from eventually migrating to more comprehensive financial platforms.

- Opportunities: The overall market trends provide a massive tailwind for MercadoLibre. Latin America’s e-commerce penetration is still in early stages – e-commerce was only about 11% of total retail sales as of 2022 (Source), far lower than in China or even the U.S.

This means there is a large runway as more shopping moves online; MercadoLibre can capture a large portion of the TAM (Total Addressable Market) which is expected to reach $160–$200 billion in e-commerce sales by mid-decade (Source).

Likewise, in fintech, the opportunity is enormous: Latin America has hundreds of millions of consumers and small businesses still not fully served by banks – even in 2021, about 122 million adults had no bank account (Source), and many more are underbanked.

As internet access and smartphones spread, MercadoPago is well-positioned to be the onboarding platform for these users’ financial lives.

Another growth area is digital advertising – MercadoLibre can increasingly monetize its platform via ads, tapping into Latin America’s digital ad market which is projected to triple by 2028 to over $5 billion in size (Source).

Every percentage point increase in MercadoLibre’s ad penetration (currently ~2% of GMV) could add hundreds of millions in high-margin revenue.

Additionally, MercadoLibre has opportunities to expand in underserved countries (e.g., Central America or the Caribbean where it has a smaller presence) or potentially even beyond Latin America in the future.

It could also deepen its ecosystem – for instance, offering new services like travel bookings, ticket sales, or deeper integration of streaming or digital content to leverage its user base (akin to how Amazon expanded into multiple verticals).

Furthermore, continuing to develop MercadoCrédito and perhaps offering more financial products (like insurance through partnerships, or investment products) can increase user engagement and revenue per user.

Essentially, MercadoLibre can grow “vertically” by adding more products to its ecosystem and “horizontally” by reaching more users and sectors, all on top of favorable secular trends in digital adoption.

- Threats: The competitive and regulatory environment poses some threats to MercadoLibre.

A major threat is the possibility of aggressive moves by global tech giants: Amazon is the obvious one, but also consider if Alibaba ever decided to invest heavily in Latin America (either directly or via an acquisition) or if Sea Limited re-escalates Shopee’s presence with more capital.

Another threat is local copycats or niche specialists undermining parts of MercadoLibre’s business – for example, a startup could focus only on grocery delivery or only on used goods, etc., carving away segments of MercadoLibre’s GMV.

So far MercadoLibre has been adept at either acquiring such companies or out-competing them, but the startup ecosystem in Latin America is vibrant (Brazilian unicorns like iFood in food delivery, or Rappi which is a Colombian all-purpose delivery app, show that local tech firms can grow fast – while not direct competitors to MercadoLibre, a super-app like Rappi could divert consumer attention and become a platform for retail in the future).

Regulatory threats are also significant: As MercadoLibre becomes a fintech powerhouse, it may face stricter banking regulations in various countries (requiring higher capital reserves for its credit business, or limits on fees it can charge).

Any regulatory move to open up payment interoperability (for example, Brazil’s central bank pushing all digital wallets to be interoperable via Pix) can reduce the moat of a closed network like MercadoPago.

Similarly, governments might enforce stricter e-commerce rules – such as requiring marketplaces to police sellers more tightly for tax purposes or consumer protection; this could increase compliance costs.

Political instability or policy shifts could also threaten: a new government could favor state-owned players or impose foreign trade restrictions that complicate cross-border commerce (an example being import taxes to protect local retailers, which could affect MercadoLibre’s cross-border sales).

Lastly, cybersecurity and fraud are ongoing threats – as the largest e-commerce and fintech player, MercadoLibre is a prime target for fraudsters and hackers.

A major breach or scandal could erode user trust, which is the bedrock of its business.

MercadoLibre invests heavily in security and fraud prevention, but it’s a never-ending battle.

In a direct matchup SWOT with Amazon in Latin America: MercadoLibre’s strengths are local integration and fintech, Amazon’s strength is global scale and a perfected model; MercadoLibre’s weakness is smaller scale and currency exposure, Amazon’s weakness is less local insight and weaker fintech presence in LatAm; the opportunity for both is a growing market, and the threat to both is each other as well as economic/political hurdles.

With Shopee, the threat is more about keeping an eye on innovative engagement strategies (gamification) that appeal to younger users.

With local players, the threat is if one of them cracks the code of combining online and offline advantages to out-service MercadoLibre in a particular country.

So far, MercadoLibre’s crown in Latin America is secure – “MELI’s crown is safe – for now,” as one analysis put it (Source).

But the competitive landscape is dynamic, and MercadoLibre will need to continuously invest and innovate to stay ahead of both global giants and homegrown disruptors.

Market Size & Growth Metrics

Easy Button:

• Latin America’s online commerce market is expanding rapidly – total e-commerce sales are forecast to reach roughly $260 billion by 2028, nearly triple the level of a few years ago (Source). Despite fast growth, online sales are only about 10-12% of total retail in the region, indicating significant runway for future growth.

• The fintech opportunity is enormous: Latin America’s digital payments market is projected to triple to $300 billion by 2027 (Source), driven by financial inclusion efforts and e-commerce adoption. Hundreds of millions of transactions are shifting from cash to digital, benefiting players like MercadoPago.

• Digital advertising in e-commerce is a nascent but high-growth segment – Latin America’s online advertising spend is expected to triple by 2028 (to over $5 billion), which aligns with MercadoLibre’s push to capture a greater share of merchants’ ad budgets (Source).

Total Addressable Market (TAM) – E-commerce: Latin America is often cited as one of the world’s fastest-growing e-commerce regions.

The COVID-19 pandemic accelerated online shopping, and that momentum has continued.

In 2023, Latin America’s retail e-commerce sales were roughly on the order of $100–120 billion, and forecasts suggest ~$160 billion by 2025 and around $230–$260 billion by 2028 (Source) (Source).

This represents annual growth rates well above global averages (high-teens to 20%+ per year).

The drivers are increased internet penetration (particularly via smartphones), improved trust in online shopping/logistics, and a young population open to e-commerce.

By country, Brazil is the largest e-commerce market (expected to hit ~$95 billion in e-commerce revenue by 2023 (Source)), followed by Mexico (in the tens of billions) and then Argentina.

These three make up the lion’s share of regional e-commerce TAM, but smaller markets like Colombia, Chile, and Peru are also growing quickly.

MercadoLibre, being the market leader, is in a prime position to capture a large portion of this TAM.

However, TAM growth also attracts competitors (as discussed).

It’s notable that e-commerce as a percentage of total retail is still relatively low in LatAm – roughly 11% region-wide as of 2022 (Source), compared to about 20% in the US and over 30% in China.

This gap signifies how much room there is for growth.

If LatAm eventually reaches those higher penetration levels, we’re talking several-fold increases in online sales from current levels.

For MercadoLibre, even maintaining its current market share in a rapidly expanding pie would result in strong growth; any market share gains would compound on top.

Within e-commerce TAM, certain segments are evolving: categories like consumer electronics and fashion have been early drivers (and are nearing higher online share), whereas groceries and home goods are less penetrated but starting to move online.

MercadoLibre has been pushing into these new categories (e.g., launching supermarket offerings, partnering with grocery chains) to expand its TAM capture.

Additionally, cross-border trade is part of TAM – many LatAm consumers buy from foreign sites (AliExpress, Amazon US, etc.).

As regional infrastructure improves, some of that volume could localize (where MercadoLibre could win it), or MercadoLibre could facilitate cross-border via its platform (e.g., allow international sellers but fulfill locally).

In short, the TAM for e-commerce is not just growing in absolute terms but also in scope, as new product categories and shopping behaviors come online.

TAM – Fintech & Payments: Latin America’s payments landscape is undergoing a revolution.

A large portion of transactions historically were cash-based, but that is changing with the rise of digital wallets, instant payment systems, and fintech services.

Reports project that digital payment revenue in Latin America will triple to about $300 billion by 2027 (Source).

This includes online payments for e-commerce, mobile wallet transactions, real-time bank transfers (like Pix), and other fintech services.

The growth rate is fueled by both consumer adoption (more people using apps instead of cash) and merchant adoption (even street vendors now often accept QR or mobile payments in major cities).

For MercadoPago, one key TAM metric is Total Payment Volume (TPV) – which includes payments on MercadoLibre’s marketplace and off-platform.

MercadoLibre’s TPV has been surging (in 2024, TPV for the full year was well over $100 billion in USD, growing strongly FX-neutral).

Considering the overall consumer expenditure in LatAm, there is still huge headroom for digital payment penetration.

Brazil’s Pix system alone processed billions of transactions in its first two years, indicating how quickly users can shift if given a convenient option.

MercadoPago competes in this TAM not only with banks but also with fintech peers; however, the market is likely big enough for multiple winners, and many consumers will use more than one service.

Another aspect of fintech TAM is credit.

Traditional bank credit (credit cards, personal loans) has relatively low penetration in Latin America – many people either don’t have credit access or face very high interest rates. MercadoCrédito’s TAM includes the vast pool of consumers and small businesses that need credit.

By some estimates, more than 70% of Latin American adults are “underbanked” in terms of credit access (Source).

MercadoLibre’s approach of lending for e-commerce purchases or to marketplace sellers is a wedge into that market.

As it gathers data, it could extend credit offers to more of its 100+ million user base.

The risk-adjusted TAM will depend on how many of those users are creditworthy or can be made creditworthy through innovative scoring.

Nonetheless, even a fraction of that population taking micro-loans can translate to a multi-billion dollar loan book (MercadoLibre already hit $6.6B).

For context, Nubank’s consumer credit card base and loan portfolio is larger in absolute terms, but MercadoLibre is catching up quickly by leveraging commerce data.

TAM – Advertising: The digital advertising market in Latin America is growing as companies shift spend from TV/radio to online channels.

Specifically, advertising on e-commerce platforms (sometimes called retail media) is a newer slice of that.

In the U.S., this has exploded (Amazon’s $30+ billion ad business).

Latin America’s digital ad spend was about $10 billion in 2022 (for all online ads) and is expected to continue double-digit growth.

MercadoLibre’s TAM for ads can be thought of as the marketing budgets of all the sellers and brands trying to reach Latin American online shoppers.

As e-commerce grows, brands will allocate more to reaching consumers at the point of purchase (i.e., on MercadoLibre or similar sites).

MercadoLibre noted that its advertising penetration (ad revenue/GMV) is only ~2%, whereas Amazon’s is ~5% and Chinese platforms even higher (Source).

Big Idea; Big Reality: If Latin America’s e-commerce GMV is, say, $100B+ and growing, a 5% ad penetration would imply a $5B+ ads TAM on e-commerce platforms in the coming years.

MercadoLibre is the best positioned to seize this, given its scale. So, one can envision MercadoAds going from a $1B run-rate to several billions as the market matures.

Moreover, overall digital ad TAM (search, social, etc.) in LatAm is projected to exceed $20B by late decade, and MercadoLibre can try to pull some share from Google/Facebook by proving that ads on its platform have better conversion for retail products.

Growth Metrics by Sector and Country: Looking at recent trends, MercadoLibre’s own results reflect broader sector growth: in 2024, items sold on MercadoLibre grew ~28% YoY, indicating more people shopping more frequently (Source).

Unique buyers were up 25% YoY.

These are important volume metrics signaling how the market is expanding in usage.

The faster growth of items sold relative to GMV (which grew 8% USD, but 56% FX-neutral in Q4) implies average order sizes affected by currency and mix, but volume of transactions booming.

On the fintech side, total payment transactions were up around 40-50% YoY, and off-platform payments (people using MercadoPago outside MercadoLibre) now surpass on-platform in volume – showing that the fintech TAM extends well beyond e-commerce.

By country, growth rates differ: in recent quarters Brazil and Mexico have often posted 30-50% local currency growth in commerce metrics, whereas Argentina, due to inflation, shows astronomical local growth but when converted to USD it’s lower (e.g., Argentina’s FX-neutral growth might be >100% in some metrics due to inflation, but only single-digit in USD).

For example, in Q4 2024 Argentina’s GMV in local currency was soaring, but in USD it was down year-on-year because the peso devaluation offset everything.

Meanwhile, Mexico was a star with ~40%+ growth in USD terms as e-commerce adoption there is in an earlier phase and rising fast (Source).

Brazil, being a more mature market, still managed strong growth ~20-30% FX-neutral.

So growth is coming from both increased penetration in mature markets and the steep adoption curve in emerging ones.

One can quantify TAM penetration for MercadoLibre: in 2023 MercadoLibre’s GMV was about $34 billion (in USD).

If the total LatAm e-commerce that year was perhaps ~$100-120B, MercadoLibre had roughly 28-30% share of all online GMV.

If the total market triples by 2028, and MercadoLibre keeps even 25% share, its GMV would triple as well (all else equal).

Naturally, MercadoLibre aims to not just keep but grow share in many markets by outpacing competitors.

The company’s ability to grow users (it crossed 100 million buyers in 2024) is a good proxy for how it is capturing more of the TAM. For fintech, MercadoPago processed about $125B in TPV in 2023.

The estimated digital payments volume (including all methods) in LatAm was larger, but with $300B digital payments TAM by 2027, MercadoPago could aim for a substantial slice, especially as it offers more services.

Its user growth (61M MAU) versus a ~400M adult population in its main countries indicates plenty of room to onboard new users.

In conclusion, the market size trends are strongly in MercadoLibre’s favor.

E-commerce and fintech in Latin America are growth stories with decades-long runways.

The main question is how the pie gets divided, but as the pioneer, MercadoLibre is positioned to capture a very healthy portion.

The company often cites third-party research in its investor materials pointing to these TAM expansions – for instance, a forecast that Latin America e-commerce will grow 54% from 2023 to 2025, or that digital payments will exceed certain thresholds.

All these indicators underscore that MercadoLibre’s core markets are structurally growing, providing a strong tailwind to complement the company’s execution.

Financial Analysis

• MercadoLibre’s financial performance has been exceptional, with record results in Q4 2024: quarterly net revenue hit $6.1 billion (up 37% YoY) and net income reached $639 million (Source).

This capped off 2024 with ~$21 billion revenue (38% growth) and nearly $1.9 billion in net profit – showcasing both high growth and improving profitability.

• Over the past five years, MercadoLibre’s revenues have skyrocketed (from ~$3.0 billion in 2018 to $20+ billion in 2024) at a CAGR well above 50%, while it moved from net losses to solid profits.

The company’s operating margin rose into double-digits by 2024 as it scaled, after years of reinvestment (Source).

• Q4 2024 details show the Commerce segment delivered robust growth (8% YoY GMV in USD, 56% FX-neutral) and improving efficiency, and the Fintech segment led growth (74% YoY loan portfolio increase, expanding take rates).

MercadoLibre’s focus on cost control and higher-margin services (like ads) lifted its net income margin to ~10.5% in Q4 2024 (Source).

Q4 2024 Results

MercadoLibre’s fourth quarter of 2024 was a blockbuster, underscoring the company’s momentum.

Net revenue came in at $6.1 billion for Q4, a 37% increase year-over-year (Source).

This beat market expectations and was driven by strong holiday season sales and continued user growth.

In fact, Q4 is typically the biggest quarter (with holiday shopping), and the $6.1B figure was nearly half of the entire year’s revenue, reflecting seasonality and scale.

Net income for Q4 was $639 million, up 67% year-over-year (excluding a one-time accounting adjustment in the prior year) (Source).

This yielded a net margin of about 10.5%, which is a significant improvement from prior years when Q4 margins were mid-single digits or even negative in earlier days.

Importantly, MercadoLibre’s income from operations in Q4 was $820 million (an all-time high), indicating that even after accounting for taxes and other expenses, the core business is throwing off substantial operating profit (Source).

Looking at segment performance in Q4 2024: The Commerce segment (marketplace, etc.) saw its gross merchandise volume (GMV) grow to $14.5 billion, an 8% YoY growth in USD – which might seem modest, but on a currency-neutral basis it was extremely strong (over 50% growth) highlighting that underlying volumes are booming once forex noise is removed (Source).

The number of items sold grew 27%, indicating more transactions even if average order values were affected by currency or mix shifts (Source).

Marketplace take-rate (revenue as % of GMV) has been rising as MercadoLibre adds services – in Q4, the take rate was well above 16% when combining marketplace fees, payments, shipping, and ads.

The Fintech segment was a star: fintech revenues grew about 60% YoY (in USD) in Q4, outpacing commerce revenue growth (Source).

Total Payment Volume processed was around $36 billion for the quarter (up ~80% FX-neutral, though lower in USD).

The credit portfolio expansion to $6.6B (74% YoY) shows management’s confidence in underwriting and the demand for loans (Source).

They did note slightly higher delinquency in short-term metrics but improved long-term delinquency, suggesting their credit quality is stabilizing even as they grow.

Meanwhile, MercadoAds revenue grew 41% YoY in Q4 to ~$300M (as noted), and reached 2.1% of GMV, which is a positive trend for margin mix (Source).

MercadoLibre’s cost structure in Q4 2024 also showed efficiency gains.

Gross profit margin was slightly pressured by a higher mix of 1P sales and the growth of credit (which carries interest expenses), but operating expenses grew slower than revenues.

Sales & marketing spend, for instance, as a % of revenue, is carefully managed; a lot of MercadoLibre’s growth is organic or via efficient performance marketing.

The result was an operating margin of ~13.4% in Q4 (excluding some accounting changes), up from 11.2% a year earlier (Source).

This shows the benefit of scale – MercadoLibre’s investments in warehouses, data centers, etc., are yielding operating leverage.

It’s also notable that free cash flow generation is strong: for full-year 2024, operating cash flow was $7.9B, up 54%, though much was reinvested in expanding the credit portfolio and capex (hence free cash flow was around $1.3B) (Source).

The company raised some debt in past years, but with improving cash flows, it is largely self-funding growth now.

Five-Year Financial Trend: MercadoLibre’s trajectory from 2019 to 2024 is one of hyper growth and a shift from break-even to robust profitability.

In 2019, MercadoLibre had about $2.3 billion in revenue and actually recorded a net loss of $172 million (Source).

The company was heavily reinvesting and facing forex issues (e.g., Argentine peso devaluation hit earnings).

2020 saw revenue jump to $3.97 billion (73% growth) as e-commerce demand spiked during the pandemic, and MercadoLibre roughly broke even on the bottom line (small $1 million loss) (Source).

2021 was a pivotal year: revenue exploded to $7.07 billion (+78%) and the company turned a small net profit of $83 million (Source).

But margins were still thin as logistics and fintech investments ramped up.

In 2022, revenue reached $10.5 billion (+49%) and net income jumped to $482 million (Source).

This was when MercadoLibre proved it could grow fast and improve profitability simultaneously – operating income improved significantly as take rates rose and scale benefits kicked in.

2023 continued the trend: revenue hit about $15 billion (+42%) and net income doubled to $987 million (Source) (Source).

By 2023, net profit margin was ~6.8%, a big improvement from near-zero a couple of years before.

And finally, 2024 saw an estimated ~$21 billion revenue (+38%) and ~$1.9 billion net income (net margin ~9%) (Source) (Source).

The trajectory shows MercadoLibre growing roughly 9x in revenue over five years, with net income swinging from negative to nearly $2 billion positive.

This five-year span also reflects a shift in revenue mix: in 2018-2019, marketplace was the vast majority of revenue, whereas by 2024, fintech (MercadoPago etc.) is around 40%.

It also reflects increased monetization: MercadoLibre’s take rate (total revenue/GMV) has risen from about 10% in 2018 to ~16-17% in 2024, thanks to contributions from payments and shipping fees and ads.

Another point is operating expense leverage: In early years, costs like Product Development (tech investments) and G&A grew slower than revenue, demonstrating scale.

However, one line that grew was provisions for doubtful accounts (as credit expanded) – MercadoLibre has managed to keep credit losses in check relative to revenue growth so far.

From an investor perspective, MercadoLibre’s financial profile has evolved from a “growth at all costs” story to a more balanced “growth + profitability” story.

Gross margins have oscillated due to mix (fintech revenues include some low-margin parts), but operating margins have steadily climbed.

EBITDA margin was around 10% in 2022, improved further in 2023, and Q4 2024 was above that.

Return on invested capital is improving now that earlier heavy investments are paying off.

The company’s equity issuances have been minimal in recent years (it did issue some convertible debt in 2020 to bolster cash during the pandemic, but dilution has been small). Thus, shareholders have seen earnings per share grow.

Indeed, Q4 2024 EPS was $12.61, wildly beating analyst estimates of ~$7.90 (Source), reflecting how far ahead the company is executing.

To contextualize historically: MercadoLibre used to trade at very high P/E multiples (as it had tiny earnings), but now with nearly $2B in earnings and continuing growth, its valuation metrics are normalizing.

The five-year stock chart mirrors these fundamentals – MELI’s stock has roughly quadrupled since 2018, in line with its revenue growth, and the market has rewarded evidence of profitability by pushing it to all-time highs in early 2025.

A quick look at segment margins (if data available): MercadoLibre’s commerce segment has seen improved contribution margins as shipping operations matured and as ad revenue (high margin) grew.

The fintech segment’s contribution margin, around 24% in 2024, is also positive but slightly lower due to costs in scaling the credit card business and promotional spend (Source).

Both segments are now contributing healthily.

MercadoLibre’s balance sheet over these years strengthened: as of end 2024, it had ~$7.5B in cash and equivalents (boosted by operating cash flow and some borrowings) and a similar amount of customer funds liability (from MercadoPago balances) on the other side, plus a growing loans receivable asset.

Debt is moderate (it issued bonds ~$1.1B in 2021 and some convertible notes).

Overall, the financial position is solid, giving flexibility for future investments or weathering macro storms.

In conclusion, MercadoLibre’s financial story is one of high-growth scaling into profitability.

The Q4 2024 results exemplify the company hitting a sweet spot: strong consumer demand, multiple revenue levers firing (commerce, fintech, ads), and improved operating leverage.

While foreign exchange fluctuations (e.g., a devaluation in Argentina or currency shifts in Brazil) can make the USD figures lumpy quarter-to-quarter, the underlying constant currency growth has been extremely robust.

The five-year trend gives confidence that MercadoLibre can manage growth and margins together – a critical point as it faces giant competitors (it shows MercadoLibre can invest where needed yet still deliver profits).

Wall Street now often compares MercadoLibre’s financial profile to that of a “mix between Amazon and PayPal, with faster growth,” which is high praise but earned by these results.

Tariffs & Trade Risk Analysis

Easy Button:

• MercadoLibre’s business can be affected by international trade policies – for instance, U.S. tariffs or trade tensions under the Trump administration (and potentially in the future) could indirectly impact Latin American economies and consumer spending, posing a risk to MELI’s growth.

• Changes in local import/export rules are a double-edged sword: Mexico recently imposed a 19% tax on low-value imports from Asia, which hurts MercadoLibre’s sourcing of cheap goods from China but also curbs competition from platforms like Shein/Temu, potentially benefiting MELI (Source).

• In Brazil, new tax rules in 2023 exempting small cross-border purchases from heavy tariffs (but adding VAT) aimed to crack down on informal imports; analysts warned this might encourage more direct Chinese competition and was a short-term headwind for MercadoLibre’s local sellers (Source).

Big Idea; Big Reality: Overall, while US tariffs on Mexico might shift competitive dynamics and consumer behavior locally, MercadoLibre’s performance remains primarily driven by Latin American fundamentals rather than US tariff policies.

Before diving into an intellectual argument, we reprise the image from the lede that plots the performance of MELI versus the NASDAQ 100 (QQQ) year to date, and at least for now, the market believes tariffs are bad for the US and good (or less bad) for MELI.

While MercadoLibre itself is a Latin American company, not exporting to the U.S., it is still exposed to U.S. trade policy indirectly.

During the Trump administration (2017–2020), there were threats and actions that created uncertainties.

For example, the U.S. at one point imposed tariffs on steel and aluminum imports from Brazil and Argentina.

Those tariffs (and threats of broader tariffs on goods) contributed to currency volatility – in late 2019, the U.S. even briefly considered restoring tariffs due to currency moves, which caused the Brazilian real and Argentine peso to dip.

Such devaluations make imported goods more expensive locally and can dent consumer purchasing power, indirectly affecting MercadoLibre’s sales.

Additionally, Trump frequently criticized NAFTA (now USMCA) and threatened tariffs on Mexico if issues like immigration weren’t addressed.

While those particular tariffs didn’t materialize, the specter of U.S. tariffs on Mexican goods or on automotive supply chains could have harmed Mexico’s economy, where MercadoLibre is growing fast.

Big Idea; Big Reality: In short, U.S. trade policy uncertainty is a macro risk – if a major trade war had triggered recessions or currency crises in LatAm, MercadoLibre would feel the pain via lower demand.

Going forward, the possibility of a return to more protectionist U.S. policies (for instance, a future Trump or similar administration) remains a background risk.

On the flip side, some U.S. trade moves actually benefit MercadoLibre’s competitive position.

One example is the U.S.-China trade war, which led some Chinese manufacturers to look more at emerging markets like LatAm for growth, increasing competition (like Shein selling directly).

But it also made Chinese goods slightly more costly in some cases.

Another interesting angle: because Mexico has a free-trade deal with the U.S., imports from the U.S. to Mexico are easier.

Amazon has leveraged shipping from U.S. inventory to Mexico.

If U.S.-China tensions push more production to Mexico (nearshoring), local supply might improve, which MercadoLibre can tap (good), but if U.S. puts tariffs on Mexican exports, Mexico’s economy could suffer (bad for consumer confidence).

It’s a complex mix.

Focusing on local trade policies: E-commerce often involves cross-border parcels, especially from China (for inexpensive goods).

Latin American governments have been trying to balance allowing affordable goods for consumers with protecting local merchants and ensuring tax collection.

Mexico (2025) – Starting in January 2025, Mexico imposed a 19% VAT on packages imported via courier from countries without a free trade agreement (like China), for packages under $50 which were previously duty-free (Source).

This measure explicitly targeted ultra-cheap imports from platforms like Shein and Temu that exploited the de minimis exemption.

For MercadoLibre, this has two sides: about 15% of MercadoLibre’s goods sold in Mexico were sourced from abroad (mostly China) (Source), so those items may become a bit pricier or more cumbersome to import (slight negative).

However, the policy hits pure-play Chinese apps even harder, leveling the field.

Analysts at Itaú BBA actually concluded the net effect is positive for MercadoLibre and Amazon, because it reduces the price advantage of Chinese sellers and likely pushes more shoppers to buy from local or regional inventory (Source).

In addition, imports from the U.S. under $50 remain duty free in Mexico (due to USMCA), which means MercadoLibre could route some products via its U.S. operations or encourage U.S. sellers – a competitive edge over Chinese platforms subject to the 19%.

Similarly, Mexico also raised tariffs on textiles and footwear (to curb Chinese contraband) – again, pushing some apparel sourcing to local channels.

Big Idea; Big Reality: Overall, Mexico’s protectionist turn in e-commerce is a positive for MercadoLibre in defending its turf, even if it has to adjust some sourcing.

Brazil (2023): Brazil faced a flood of direct-to-consumer imports from China (via AliExpress, Shopee, Shein).

The Brazilian government in mid-2023 announced enforcement to end tax evasion on these imports.

They proposed removing a tax exemption for imports under $50 between individuals (which companies were abusing by labeling packages as gifts) and instead instituting an official $50 tax-free threshold plus a 17% VAT on imports below that (with normal duties above) (Source).

While final details shifted, the essence was to ensure Chinese e-commerce companies paid taxes.

BofA analysts at the time downgraded MercadoLibre’s stock, suggesting that formalizing the $50 exemption could encourage more cross-border players (since now below $50 is clearly legal with just VAT) and make it easier for consumers to buy direct from abroad, raising competition for MercadoLibre’s local sellers (Source).

In effect, if a Shein dress under $50 now just pays 17% VAT instead of being outright illegal, Shein can ship more confidently.

MercadoLibre might see some pressure in categories like low-cost apparel.

However, MercadoLibre also pivoted to benefit from this by accelerating its own cross-border offerings – it can use its Mexico-US corridor or its global seller program to bring goods in and comply with the new rules, thus competing with Shopee/AliExpress on equal footing.

Another risk is that if global sellers get easier access, MercadoLibre’s take rate on those sales might be lower (since those could occur off its platform too).

But MercadoLibre’s scale means many of those sellers would prefer listing on MercadoLibre Brazil with the infrastructure, rather than relying solely on direct-to-consumer routes.

Still, it’s a nuanced risk – trade rule changes require MercadoLibre to adapt or lose share.

Tariffs on Imports/Exports: For MercadoLibre’s own operations, tariffs could affect its cost of goods sold for any first-party sales.

For instance, if it imports electronics to sell directly, tariffs would raise costs.

Also, if tariffs make products expensive, consumers might reduce discretionary purchases.

Another angle: export opportunities.

MercadoLibre launched a program “MercadoLibre Global Shipping” allowing Latin American sellers to export abroad.

If destination countries impose tariffs, that could hamper Latin sellers (though this is currently a small portion of business).

Logistics and Customs Delays: Trade policies also include customs processes.

More stringent controls on packages (to enforce tariffs) can slow down cross-border shipping.

If buying from abroad becomes slower or riskier, MercadoLibre’s value proposition of fast local delivery shines – again a competitive dynamic to monitor.

MercadoLibre might need to re-route or adjust fulfillment for cross-border items depending on policy changes.

It’s already been investing in local inventory to mitigate these risks (e.g., encouraging Chinese merchants to hold stock in Brazil via its fulfillment centers, so items are already imported in bulk and cleared).

U.S.-China Relations Impact: While not directly about MercadoLibre, a wider U.S.-China trade rift can impact supply chains.

Latin America might see cheaper Chinese goods if China diverts exports or the opposite if costs rise.

Also, any global economic slowdown from trade wars would hit consumer spending.

So far, Latin American e-commerce has been resilient despite these external issues, but it’s a consideration.

In summary, MercadoLibre must navigate a patchwork of trade regulations: U.S. trade policy (with Latin America caught in between major powers), and Latin countries’ own tariff/vat regimes for e-commerce.

The recent trend is governments wanting to tax e-commerce imports more, which could slightly raise costs but generally helps MercadoLibre by reducing unfair competition.

A risk would be if a country imposes an e-commerce-specific import restriction that hurts selection on MercadoLibre.

Alternatively, trade integration like expanded free-trade agreements can help MercadoLibre get goods more cheaply.

The company’s strategy includes engaging with regulators (MercadoLibre often publicly supports measures to “level the playing field” against gray imports) and adjusting its logistics network to whatever the optimal cross-border routes are under new rules.

Mercadolibre’s diversification across countries also means a change in one country (like Brazil’s rules) doesn’t derail the whole company, but it adjusts locally.

Finally, it’s worth noting that MercadoLibre itself is often seen as a champion of regional commerce – it benefits when Latin American countries trade more with each other (e.g., a Brazilian seller reaching a Chilean buyer through MercadoLibre).

Tariffs between Latin countries (Mercosur, etc.) can affect that.

So far, intra-LatAm e-commerce trade is small but could grow if integration improves.

Any Mercosur or Pacific Alliance trade agreements that reduce tariffs could allow MercadoLibre to unify markets more (for example, shipping goods from Brazil to Argentina with less friction).

These are potential long-term upsides if regional trade barriers fall.

Conversely, protectionism within LatAm (like Argentina’s import restrictions) can limit MercadoLibre’s ability to offer the full range of products in a country.

Argentina, for instance, has strict controls that sometimes limit imports of certain goods – MercadoLibre’s Argentine site might then have less availability for, say, imported electronics, compared to its Brazil or Mexico site.

This can push Argentine consumers to informal markets.

Thus, MercadoLibre also contends with each country’s trade posture: open markets favor its cross-country scale, closed markets can constrain it to domestic supply.

Given current trends, most large LatAm markets want to tax but not outright ban e-commerce imports, so the likely scenario is manageable for MercadoLibre with careful compliance and strategic adjustments.

Macroeconomic & Political Stability

Easy Button:

• MercadoLibre’s performance is influenced by Latin America’s economic swings – high inflation and currency devaluations (particularly in Argentina) pose a risk by eroding consumer purchasing power and distorting financial results when converted to USD (Source).The company has managed to remain profitable even in turbulent economies, but FX volatility can mask underlying growth.

• Political conditions in its key markets (e.g. Brazil, Mexico, Argentina) are generally stable for business, though each has unique risks.Brazil’s recent government transition has so far been market-friendly, but policy changes like new taxes or labor laws can impact costs.

Argentina’s volatile politics (e.g., a new administration vowing radical economic reforms) introduce uncertainty in MELI’s second-largest market.

• MercadoLibre mitigates some macro risks by operating in multiple countries and increasingly pricing services in local currencies.

However, currency risk remains significant – for instance, a sudden peso devaluation in 2023 shrank Argentina’s contribution to USD results (Argentina went from over 50% of MELI’s EBIT to 15% after a devaluation) (Source).

Latin America is known for economic volatility, and MercadoLibre’s fate is tied to these macroeconomic currents.

Inflation and Currency: Several of MercadoLibre’s markets have experienced high inflation in recent years – Argentina being the extreme case with inflation over 100% in 2023.

High inflation often leads to currency devaluation.

For MercadoLibre, this creates a few challenges. Firstly, consumer purchasing power can be hit.

If prices of basic goods soar, consumers have less disposable income for online shopping.

Interestingly, e-commerce sometimes outperforms in inflationary times because people hunt for deals online or need to buy goods quickly before prices rise more.

MercadoLibre in Argentina, for example, has seen volume growth despite economic crisis, as people use e-commerce even as a hedge (buying durable goods as store of value, etc.).

Secondly, when local currencies devalue against the US dollar (which is how MercadoLibre reports financials), it can dramatically reduce the reported growth.

A clear example: in August 2023, Argentina devalued its peso ~20% overnight as part of an IMF deal.

In MercadoLibre’s Q3 and Q4 results, Argentina’s contribution in USD dropped, and overall YoY USD growth was dampened, even though in local terms Argentina’s sales were booming.

As Reuters reported, Argentina’s devaluation hurt what was an otherwise highly profitable business – Argentina had been contributing disproportionate profits (due to high interest rates on float and pricing power) but once converted to USD, a chunk evaporated (Source).

Management noted that Argentina’s share of EBIT fell from over 50% to 15% after the devaluation (Source).

This illustrates a key risk: MercadoLibre can generate strong local results but if a currency crashes, it loses dollar value.

The company combats this by pricing strategies – they frequently adjust prices (commissions, etc.) for inflation and also hold some revenues in USD-linked instruments when possible.

They also manage a treasury strategy where they quickly convert excess local cash into hard assets or loans to avoid holding depreciating currency. But they can’t fully escape FX risk.

Interest Rates: Latin American interest rates have been high (Brazil’s base rate was in double digits until recently).

This has two effects: positive – MercadoLibre earns significant financial income on things like MercadoPago balances in places like Brazil (earning interest on float at, say, 13% yields boosts fintech revenue), and it can charge high interest on MercadoCrédito loans (because prevailing rates are high).

Negative – high rates can dampen credit demand and consumer spending, and increase the cost of capital for MercadoLibre or its sellers.

In 2022-2023, Brazil’s high rates meant MercadoLibre’s credit business had to be cautious to ensure borrowers could handle rates.

Now rates are easing (Brazil cut to ~11.75%, likely going lower), which might spur more borrowing and consumer spending – a tailwind.

In contrast, Argentina’s interest rates (over 70%) basically mean credit is very expensive and mostly short-term.

MercadoLibre navigates these by tailoring credit offerings per market.

Macroeconomically, as long as inflation trends downward in places like Brazil and Mexico, it should help MercadoLibre by improving consumer confidence and lowering its own cost for financing growth.

Country-by-country political landscape: